Post-purchase rationalization: The tendency to retroactively ascribe positive attributes to an option one has selected and/or to demote the forgone options.

It’s been quiet around here, but I have finally been inspired to write an article.

You could be forgiven to think that I would write about the exemplary performance of Greggs Plc which have gained 130% since I first tipped them in 2016 .

Alas, it would appear that I am much more of a critical thinker.

Instead I will focus on ironing out my mistakes, not patting myself on the back.

Today I will focus on my investment in Card Factory Plc and will dissect why a critical dose of post-purchase rationalization bias blinded me from the clear deterioration in business fundamentals.

The decision to purchase Card Factory Shares

I was first convinced to buy Card Factory shares in September of 2017 after what I thought was market over reaction causing the share price to drop 15%. I saw that the business had very strong cash generation, great margins and seemed to have a clear edge on rival Clinton cards and supermarket stockists.

During this period, I saw predicted that Card Factory’s margins would be stable and that management would expand further into the online market, but the investment clearly hasn’t worked out with a 60% decline on my purchase price.

To be fair, I predicted much of the problems Card Factory would face back then, in my original article on Card Factory shares I noted the difficulty that the retailer would have in maintaining margins due to it’s price-orientated model but I was convinced that the company would succeed in cross-selling higher margin products and that a lid could be kept admin expenses (mostly business rates and the wage bill) as a proportion of revenue as the increase in online sales would dwarf the increases in admin expenses from physical store openings.

I noted;

“I see clear opportunities ahead with a very impressive 30% growth in online Sales (although from a low base) and the expanding revenue an encouraging sign of demand for Card Factory’s products. Although the price of cards have clear price ceilings, there is always the probability of an increased focus on cross-selling products such as balloons, mugs e.t.c where Card Factory can afford to pass the costs on to the consumer.”

So where did it go wrong?

- Card Factory’s management continued to expand the number of high street stores to grow revenue despite declining footfall. This means Card Factory is consistently ‘working harder’ to convert revenue into free cash when compared to online sales.

- I failed to notice the poor margins on cross-sold products.

- Card Factory’s management continued to pay out special dividends instead of putting the money to creative use.

Now, let’s work through this list together.

Card Factory’s management continued to expand the number of high street stores to grow revenue despite declining footfall

“Revenue is vanity, profit is sanity”

Unfortunately, the quality of Card Factory PLC’s management team pales in comparison to the great names running other constituents of my stock portfolio, the likes of Lord Wolfson of Next PLC for example.

Instead of taking prudent measures to protect margins and the bottom line management has embarked on a 50-store-a-year expansion program that has weighed heavily on net cash generation and net margins despite management’s claims to the contrary.

Astonishingly, management appear somewhat unaware of the margin decline or, as I would suspect more likely, are polishing a turd in the hope that the casual investor won’t dig too much in to the numbers.

Here’s what they had to say regarding margins in the 2019 half year report;

“Our margins remain strong and, whilst we have seen some impact from National Living Wage and the additional cost of holding increased stock levels (for Brexit contingency planning, investment in new lines and the acceleration of seasonal buying), we remain on track to deliver another year of business efficiencies.”

Strong margins, really?

I crunched the numbers and the decline in both gross and net margins should certainly worry investors despite management’s assurances to the contrary and I would certainly hope that alarm bells are ringing internally.

Such a blase attitude from management in the half year report worries me an investor.

See below the clear deterioration in both gross and net margins (line graphs) against revenue growth (bars).

We can see where they hype from the initial IPO came from with very strong net margin performance in 2016 followed by dismal year after dismal year. It may be worth noting that Karen Hubbard became CEO in 2016 and has evidently failed to steer the ship prudently.

Management has attributed the decline in net margin to increasing store costs, falling high-street footfall and increases in the national living wage, three valid factors in my opinion. I would add to these factors worsening product mix with revenue growth being driven by new store openings and volume. In other words, Card Factory are opening more stores but are selling less high-margin items.

It is startling therefore that management’s answer to these problems is to continue to open more stores on the declining high-street thus increasing the administrative expenses of the business and expanding on the very problem they note as being responsible for poor performance.

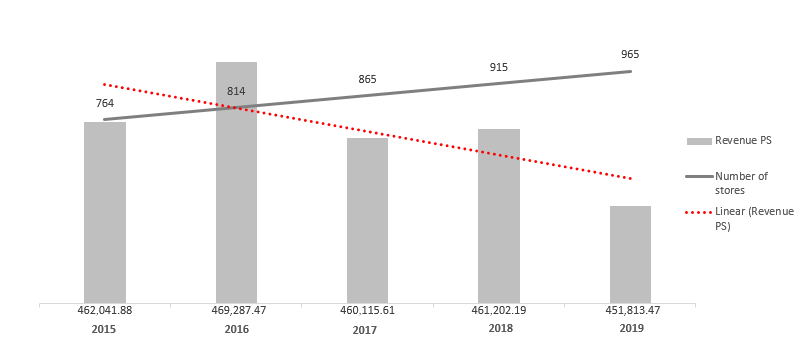

The below graph juxtaposing the number of stores and the revenue per store does more than words could to illustrate this dead-end strategy.

Obsession with Special Dividend

When businesses run out of ideas on what to do with spare cash they pay special dividends.

There’s no denying the significant sums of free cash that Card Factory continues to throw out despite margin declines.

As illustrated below, despite management’s best efforts to labor the business with increased admin expenses my FrugalStudent FreeCashFlow measure (A fancy name for how most calculate FCF which is Cash from operating activities – Capex) still shows healthy free cash generation of £56m in 2019 and healthy generation into 2020 and 2021 on a simple linear forecast basis.

With all this free cash one would imagine that management would find some use for it.

Now, I’m the first to criticize large vanity acquisitions and the effective burning of shareholder’s cash but one would feel that the pausing of high-street store openings and a heavy focus on online sales would have been a prudent avenue to put this cash to use.

Doing so would have lightened the load added on to the company’s admin expenses and presented a healthier net margin position.

The below graph displays the cash flow position after dividends in each year

I wonder where Card Factory got the money to open stores and pay dividends larger than their free cash flow?

Ah yes, good ol’ debt!

Let’s take another look at that graph but with long term debt added in.

Eagle-eyed readers would not in return that total assets have increased at a similar pace and that leveraging the balance sheet in such a way isn’t uncommon.

True. But with declining margins and a sagging bottom line, cash will increasingly be chewed up to service debt that will eventually need to be repaid from the declining free cash generate by the business.

Nevertheless at just 5 x 2019’s FS* FCF total debt isn’t too much of an issue as long as investors see a return from the 130m lumped on to long term borrowing in 2019 and dismiss the prospect of reviving special dividends in the near to middle future.

In short, management have mortgaged today’s business to pay out special dividends that the future business will have to repay.

I certainly predict on this basis that CEO Karen Hubbard will leave the business, passing her failed legacy on to someone else to deal with à la Andy McCue of The Restaurant Group.

A glimmer of hope

In November, Card Factory started supplying some Aldi stores with cards under the ‘everyday value’ brand with the view to supplying 440 current stores in the near future. Price sensitivity will be of key importance though with the other half of Aldi’s store estate being supplied by Card Factory’s rival IG Design group.

If my suspicions are correct, Aldi will pit both companies against each other in an aggressive race to the bottom once volume has been established through the stores. I do expect however that Card Factory’s vertically integrated model would give it an edge in such a scenario and hopefully will succeed in pushing out IG Design. The best businesses, however, don’t need to compete.

Card Factory also announced the imminent roll out of its card offering to The Reject Shop’s 360 stores in Australia, the logistics of which appear somewhat perplexing. We will have to wait and see what results, if any, this partnership yields.

These are exciting developments and should have been sought as an alternative to the overzealous store expansions which will only increasingly labor the company’s bottom line.

Conclusion

What was once hailed as a cash-generative high margin business is generating less cash and has lower margins.

The main lesson to learn from the purchase of Card Factory shares is that one should only ever buy businesses an idiot could run. A investment worthy business is one with such an ingrained competitive advantage that it can resist poor business decisions and leadership. Card Factory evidently isn’t one of those businesses and should not have been purchased.

The 60% decline in share price since my purchase is completely justified and it is clear that Card Factory possesses no economic moat despite historically strong cash generation.

Moving forward, I will continue to hopelessly hold the shares over the medium term in hope that management shift focus to their online offering, pause the store roll out and seek other retail partnerships, hopefully stores with more premium offerings where margins would be more robust. This could be done with an increased focus on premium card ranges.

In my opinion, as a humble investor, Card Factory could take the following five steps to turn performance around for the benefit of shareholders.

- Pause the store roll out and invest in efficiencies in existing stores that will put a lid on rising administrative expenses.

- Focus heavily on driving volume online where costs are lower.

- Roll GettingPersonal.co.uk into Cardfactory.co.uk to cut costs and maintain focus.

- Karen Hubbard should step down as CEO

- Card Factory should continue to seek retail partnerships and should en-devour to launch a more premium card range with a premium retailer.

As always, I’m interested to know if you hold Card Factory shares or are considering selling.

Are Card Factory shares a buy or a sell here for you?