The price-to-earnings ratio is the most commonly used, but also the most commonly miss-understood ratio.

You look at a stock’s P/E ratio before buying right?

The conventional p/e wisdom goes something like this.

“Typically anything under 15 is a bargain and anything in the 20s is just way overvalued”

But following such ‘wisdom’ will leave your portfolio lagging.

I have experienced this first hand.

Unfortunately, many new investors and even some experienced ones, are probably looking at P/E ratios the wrong way.

Now, that may come as a shock but by taking a few minutes to read this article you will avoid the most common P/E ratio mistakes and you’ll learn how to properly ‘read’ a P/E ratio.

Priceless information.

This article will focus on four key P/E ‘themes’ that will help you categorise most stocks just by looking at the P/E.

Here are the themes.

- The P/E that tells you nothing (very low or very very high)

- Relatively high P/E (20-30)

- Very high P/E (50+)

- The genuine value P/E

1. The P/E that tells you nothing

I watched a Youtube video a few months back and it made me a tiny bit mad.

It was a video of a guy tipping US Steel stock as a buy.

Nope, nothing wrong with that – but what got me was how he specifically drew attention to the ‘crazy low’ price to earnings ratio.

It annoyed me so bad, I even made a video response (https://www.youtube.com/watch?v=3-AqboHF9fQ).

Not because I don’t like US Steel or even people ‘tipping’ stocks on Youtube.

I responded because it was obvious he didn’t understand P/E ratios and was miss-leading new investors.

Before I learnt about P/E ratios in depth I would have been attracted by this low P/E too!

Hell – I may even have made a video tipping it too!

But, here’s why you should never use P/E alone to value stocks.

It turns out that US Steel is a cyclical stock, even worse, it’s a commodity.

Unless you have some kind of professional insight into the field a commodity is in – and lets face it, most investors don’t have this insight – I’d stay well clear of using P/E as a metric to measure its ‘value’ or investment potential.

So, why is looking at the P/E ratios of cyclical stocks, in my opinion, pointless?

It’ll be easier to explain with an example so let’s take a look at US Steel and take it from there.

US Steel is in the commodity business – Steel.

A symptom of being in the commodity industry means that their business costs depend heavily on the price of ore and their profits depend on the supply and demand for steel.

There is also often excess capacity as there are high barriers to exit from the industry.

Once you build the blast furnaces they’re pretty expensive to close down and then start up again.

Not something I want to be investing in.

But WOW – THAT 6 P/E LOOKS SO CHEAP!

Ermmm, here’s why it’s not.

US Steel’s earnings YO-YO so heavily that the P/E ratio becomes meaningless.

Just take a look at the EPS figures below;

There’s no steady trend of decline or progress here.

Who knows what the earnings for 18/19 will be?

The worst thing is – there’s very little US Steel can do to improve the situation.

They have little control over earnings and thus they are evidently extremely hard to predict.

If anyone can take any useful information for informing a buy/sell decision from this, drop me a comment, I’d love to know!

My main lesson has been to avoid such stocks since I have no expertise in them and they are notoriously hard to value.

My advice? Stay away from such cyclicals.

2. The relatively high p/e

Now and again you’ll come across a company that you really like.

For me these stocks are Visa, Mastercard, Facebook and more.

I spotted Visa years ago but didn’t pull the trigger.

Why? Well….. they seemed expensive.

But I soon learnt that there are ‘expensive’ stocks out there deliver tremendous returns, despite constantly appearing ‘expensive’.

I’ll talk about Visa here – since I now own the stock.

I first looked at Visa back in 2015 at around $65.

The P/E back then at TTM? Well 65/2.16 = 31.56

Wow, to me back then, a so called ‘value’ investor, that was just too expensive.

After all – there’s no guarantee of those future returns will materialise.

Yet here we are, in 2019 and the P/E remains around 30 and the share price has more than doubled.

I bet you’re thinking just what is going on here?

The penny came to drop in early 2018, and I finally bought the stock after reading The Little Book That Builds Wealth & Invest in the best.

Believe it or not some stocks deserve higher valuations and their P/E will simply track their rise in earnings.

But we do have to watch out since there are some stocks at 20/30 P/E that are just plain overvalued.

So how to I weed these out?

I stick by these three rules.

Any stock commanding a high valuation must;

a) Have an economic moat

b) Have very strong margins (Usually hand in hand with a)

c) Have a clear and predictable pathway to increasing EPS

Well, to begin with, Visa certainly has an economic moat, being one of only three main players in the payments game and boasting eye-popping operating margins of over 60%!

Earnings history also showed a very smooth upwards march dating back 10 years to 2009 with the only stalling in EPS growth being due to one-off expenses and drops in other operating income, not from core operations that quickly recovered.

The key question that must be asked here is,

Does the quality of these earnings and the security of future growth warrant a 30 P/E?

Only you as an investor can answer that question.

For me?

It’s a yes!

3. The very high p/e

Now we step into scary P/E territory.

I only have one example of a ‘very high p/e’ stock in my portfolio and that’s UK Tonic water maker Fevertree which sports a breathtaking (and not in a good way) P/E of 68.

I think I need to sit down.

I own this!?!

One must be very careful with such companies and my rules for such companies are far stricter.

Here they are;

Any very high P/E company must have;

a) An economic moat

b) Very strong margins

c) Strong history of high double-digit revenue growth.

d)A small market cap

e)High ROCE

As we’ve been over a/b before, let’s focus on points c, d and e.

Why am I focusing on revenue with such high p/e companies?

After all, “Revenue is vanity, profits are sanity”

Well, we would hope with such small companies that money is being ploughed in to expansion and this may hurt the bottom line over the short term.

For example, we may have high selling expenses as products are heavily promoted into new markets.

The only way to try and figure out if the company can maintain this revenue growth is to research into their market (tonics in Fevertree’s case) and to keep a very close eye on progress relative to industry size.

One must also look out for signs of retaliation from existing industry competitors that will drive down margins. (Reading Porter’s Competitive Advantage will help with spotting such moves).

For example, as a Fevertree owner I look very closely at how the company is fairing in the US as this will house most future growth and I also keep an eye on what UK competitor Britvic is doing.

In Fevertree’s case, all currently appears in order with revenue growing nearly 9x in four years.

But – just remember that the bigger a company gets, the harder it’ll get for that revenue figure to grow, hence rule d.

This rule speaks very much for itself.

If you see a company at a £50bn valuation trading at 60 p/e, it’s time to get very skeptical.

That means that the company would have to triple in value to a huge £150bn to mean that you would have paid 20 p/e for your stake in the company at the time it had tripled.

Factor in the time value of money (your money today being worth more than the same sum in 3-5 years) and your purchase must have to perform miracles to have paid off.

But hey, this has sometimes happened!

On the other hand, when we consider that Fevertree has plenty of room left to grow in the US tonic market (if the expansion is successful) then it may not be too ridiculous to envisage the current £3bn valuation growing to £9bn or one of the ‘big dogs’ swooping in to buy this premium brand (Coke, Diageo, Unilever?).

Right, so what about rule e?

What is ROCE and why am I looking for a high ROCE?

The simplest way to explain ROCE is by using a lemonade stand analogy.

Imagine you have a lemonade stand and all is going well.

You decide to invest £100 in order to expand your stand. This £100 could come from equity (share issues and retained earnings) or from taking on debt.

From that £100, you are able to generate £200 in income.

This means that your ROCE is 200%

200/100 *100 = 200

(Yes I know that this is a VERY simplistic example but it explains the concept well).

For such small companies with the need for us to see our investment grow rapidly in size, then we need to know that the money the company is pumping in to its expansion is really paying off!

Low ROCE would indicate that management is getting desperate and is pumping money into low-quality projects.

This often happens as growth slows and management scrambles for any way to keep investors happy and the share price moving upwards.

As we can see, £1 employed in 2013 would earn the company back £1.05 in 2013

A £1 employed in 207 would earn the company back £1.41

Now – that’s what we like to see.

BUT – we should monitor this trend in case of a sudden drop off due to desperate management and deteriorating conditions for rapid growth.

All that being said, my investment in Fevertree is a huge roll of the dice and I have only invested money that I could face losing 100% of.

Make no mistake, one or two bad earnings reports would see this stock half, or even worse!

4. The genuine value P/E

Now and again we get to see a stock trading at a low P/E compared to its own 10 year history and the wider market.

Of course, there are often reasons for this and there are seldom bargain basement stocks without an ora of negativity surrounding them.

A consensus wouldn’t make a market now would it.

My favourite examples of the genuine value P/E is Apple, which is currently at a 14 P/E and Next Plc which is currently trading at a 11.7 P/E.

We’ll focus on Next since there’s already plenty of content discussing Apple over at Seeking Alpha.

As recently as 2016 Next was trading at a 15.6 P/E.

As high as 17.3 in 2015.

Today? 11.7.

Now that alone doesn’t make Next a buy.

Maybe there has been some fundamental deterioration in the business.

We must first look into the stock to learn its story.

Doing our research we find out that Next was seen as a FTSE darling, a very cash generative business with a progressing dividend along with generous stock buybacks.

Here’s a company rewarding shareholders.

Taking a glance at Next PLC’s margins gives us an insight into the strength of a company.

I wonder whether this new lower P/E is down to intense competition in the fashion space?

Well, it wouldn’t seem so.

Next has managed, remarkably, to keep tight control on its operating margins.

This may be a sign of some sort of, admittedly narrow, economic moat.

Now adding the headlines of retail gloom together with some investing knowledge it becomes obvious where to look.

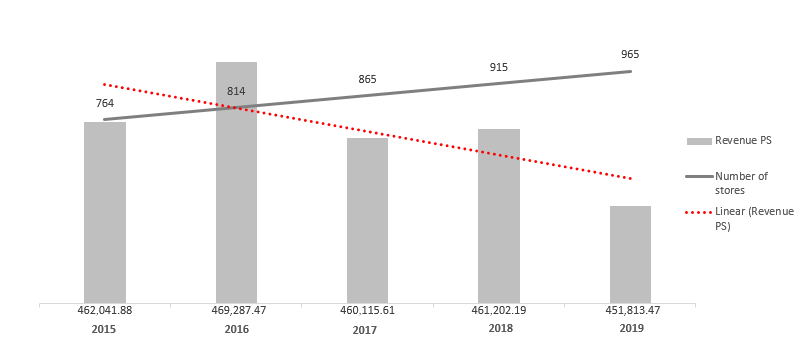

While negative industry sentiment is down to some of the drop in valuation, the other reason must surely be the downward trend in revenue (turnover) from 2016 to 2018 and the drop off in operating profit.

Some vertical analysis shows what’s going on here in a much more clear manner than taking the figures at face value.

This analysis shows each line item as a percentage of revenue.

While the first table shows the downward trend of revenue, this second table shows the upward trend in expenses, most notably from 2017 to 2018.

This ‘squeezing’ is evidently putting investors off.

But, for me, this is no problem as every business will experience squeezes every now and again.

Especially in industries such as fashion.

When we balance the cons out with what Next offers, I believe we have a case of ‘genuine value’ here.

Next offers a very safe 3.24% dividend yield and huge cash generation that is being used to buyback shares.

On top of this, despite some big retail companies closing stores, cutting margins and going bankrupt, Next has managed to maintain its operating margins.

Debenhams is down 88% this year, House of Fraser went bust and New Look is closing 85 stores.

Next remains calm and robust, even opening stores.

So, what makes a ‘genuine value’ P/E well, it’s more nuanced than just screaming ‘Value’ at low P/E stocks.

It’s about doing what I did above in order to understand the low P/E and to deem whether it’s reasonable or not.

Conclusion

So there we are.

My P/E rules all laid out.

These rules took me years to develop through hours and hours of reading and many nasty experiences.

If you have enjoyed this article then it would be great if you could share it with friends who may find it useful.

You can also follow me on YouTube here: https://www.youtube.com/channel/UCsevxoeAwjaBmie4TxEAp7Q?view_as=subscriber

Cheers!

Lewys Thomas,

Frugal Student.

After all, the prospect of a miracle turnaround by Co-founder Julian Dunkerton (pictured left) is an attractive one. Superdry isn’t a brand that’s going to disappear anytime soon, even if it is as old and tired as I suspect.

After all, the prospect of a miracle turnaround by Co-founder Julian Dunkerton (pictured left) is an attractive one. Superdry isn’t a brand that’s going to disappear anytime soon, even if it is as old and tired as I suspect.